How ESG can help drive a higher valuation of a sector critical to the world’s transition to a sustainable future.

The following article is an edited version of the speech I made at Mines & Money.

I think we should all start the year with this paradigm shift firmly in mind.

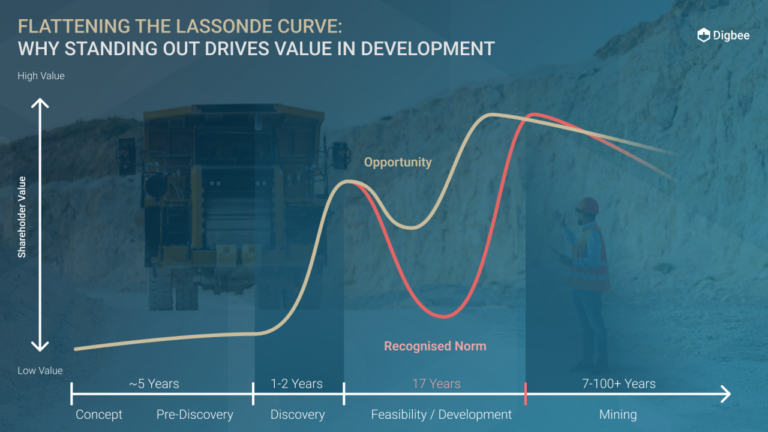

The mining industry carries the hope of the world

For many, you would be excused for not fully respecting this, given the general rhetoric and the fact mining wasn’t included in the COP26 programme. Yet mining carries the capability to deliver the transition to a sustainable future and the opportunity – for industry stakeholders and the world at large – is there for the taking. It does so from a position so deeply damaged that there needs to be a new beginning for an industry as old as industry itself.

BHP’s forecasts see the need in the next 30 years to:

- double copper production

- increase nickel output 4 times

- produce twice as much steel as consumed in last 30 years.

The industry will continue to dig holes, explore in challenging areas of the world and engage with communities, NGO’s and governments all around this great planet. If these fundamental pillars of output growth and mining are to coexist, they need to be financed in a new world of investment. From where we stand today this is looking increasingly challenging for those that require outside financing.

Alongside oil and gas, mining is the worst perceived industry on the planet. Perception of brown industries is seeing a growing cost of capital. For example:

- A Bank of America report outlines that longer dated debt issuance amongst oil & gas sector is now less prevalent and new issue coupons are 50-70bps higher than investment grade.

- The same report also highlights the increasing spread of cost of capital within materials based companies, from those that are high emitters to those that are not.

The winds of change are upon us. The question is:

How big is this: are we in a bubble or just starting out?

Let’s put the answer in numbers:

In the year to date:

- 25% of all emerging market bond flows have gone into ESG

- This increases to 63% in Western Europe, amounting to $275bn total funds under management

- This decreases to just 4% in the USA – but think of the total aggregate when this starts to catch up – It’s already at $90bn and the trend is exponential.

It is estimated that $173tln investment is required by 2050 to address climate change in energy and infrastructure. This year will see $1tln in green bonds issued – we are only at the starting blocks of this process.

What is happening in the bond market is being replicated in equities:

- 1 in 8 funds are now ESG,

- There are now three times more funds under management in ESG than there were in January 2020

- The inflows remain exponential.

The mining sector must start to differentiate itself. It must find a means to credibly prove its actions are real. It must demonstrate a new modern attractiveness for investment if we are to avoid a sector wide increase in the cost of capital and increasing exclusion from mainstream investment.

We must start changing the old narrative.

I hear many skeptics thinking that this is just not possible, that the sector will continue to bumble along as it has for decades and centuries. The world needs our resources and thus it will all sort itself out. Small companies won’t be affected the same as large ones… but this is wrong! Doors are closing.

A particular example of this came last week, when the head of mining at a major Australian lender told me that they are no longer putting any extractive company through their credit committee. The reason they gave was reputation: they just don’t have sufficient credible data to present against NGO claims.

Given the very scale of this changing landscape, the big picture is clear:

ESG has gone mainstream

A changing investment landscape and capital flows will increasingly restrict investment to those sectors and/or companies that cannot credibly demonstrate a commitment to a sustainable operation – well beyond just emissions. It’s just easier for investors to say no.

Significant change has already happened

The mining sector has been changing for decades: regulations since Bre-x have shown huge improvements in governance; health and safety improvements are lauded across other sectors; water management is well established in many jurisdictions; social engagement has shown many positive steps in recent years. But all this has gone largely unnoticed outside the sector itself.

ESG is a communication device

Here is the key: ESG in all its different clothes is also a communication tool. A tool that – if the data is credible – can begin to promote an industry for the very good that it does through the critical products it produces; for the engagement and investment in communities it provides; for the jobs it creates and, ultimately, for the planning of a long term sustainable ecosystem well beyond that of a mine itself.

Hindsight is a wonderful position but if I may give a real life example of the opportunity ESG presents, when Central Asia Metals announced a tailings spill in September 2020, their share price fell 20%. They handled the issues on the ground in the same way they would have done before, yet this time they communicated openly and transparently to stakeholders and shareholders, turning a potential PR disaster into a positive with enhanced reputation and a share price that quickly recovered.

The impact of ESG on the ground

Having explained the scale, we need to understand some of the changes which will impact mining companies on a day-to-day basis.

Firstly, this is going to affect every company, private or public, big or small. Larger companies, as seen by virtually every investor presentation, are already fully engaged: short and long term strategies are being overhauled; policies and procedures are evolving constantly to keep up with changes; capital allocation is directly impacted; financing strategies are now directly influenced by sustainability functions.

Secondly, investors are responding to a regulatory drive to divert capital to businesses that will help rewire the economy to address climate-related challenges. In the UK, for example, the regulators are redefining the role of the investment industry, incorporating the need to deliver socially useful value as part of the investment process. Your Roladex of fund manager contacts should be supplemented with stewardship teams, as there are three in this relationship now, not just two.

If this was just an access to capital issue then this would be easier to understand. But modern finance through the lens of ESG is looking further to understand the impact of changing stakeholder expectations across the value chain. Access to market for end products and social license to operate are becoming increasingly relevant to strategy discussions as the rules of the game on carbon intensity change. The valuation of your company will become increasingly linked to the measurement of this and all ESG topics.

Most company managers will likely be able to hold their heads up high when it comes to social license, as the mining industry has been ahead of the curve on this. Going forward, stakeholder engagement in this area will become more public, there will be greater demands on the company to become more transparent, which raises both opportunities and possible threats. But transparency allows the company to build trust and provides a platform for engagement with a wider range of stakeholders, including NGO’s and other potential activists.

Perhaps the area most challenging to acknowledge for an exploration company, let alone a world that requires difficult to find resources, will be knowing how far this discussion goes when it comes to access to market. Will the cost of capital for a mine that requires a long supply chain or high emitting processing be an obstacle for financing relative to other assets nearer to market or cleaner to produce? I’ve focused on the negative here but the opposite is also equally true for assets at the other end of spectrum.

For an exploration company, wherever you may be located, identify the options available early, provide planning to minimise emissions in any future development, plan early for positive nature impact, strengthen your local engagement with transparent disclosure. There will be a cost:benefit question asked, much of what is required will cost but financial markets are beginning to differentiate those industries or companies that deserve capital and those that don’t.

Different jurisdictions have different language, some are moving slower, others faster, but the message and trend is clear: boards of directors have obligations to consider sustainability as part of their oversight. Nick Stansbury, well known fund manager in the mining industry and Head of Climate Solutions at Legal & General, stated recently in a discussion of the changing paradigm of investing:

Coming back to the investment process. Mainstream funds carry out ESG screening as standard. Any identified risks will require stewardship teams to define whether the management have appropriate plans to improve or the company will be blacklisted. We have to accept, rightly or wrongly, that mining companies will typically attract the need for review.

Whether you are a CEO, chairman, private or institutional investor you want to see a rising share price, you want the market to justify the effort and value being created. Discovering new resources and developing a mine now also requires transparency in the way the company goes about that discovery or plans its future operation.

The weight of money behind a shifting paradigm of investment cannot be ignored: there will be winners and losers, there will be those that choose to embrace change and those that will not.

So how do we ensure the sector encourages new investment?

For decades, the universe of funds investing in the sector has been limited to the ebb and flow of the price cycle. It’s different this time, it’s fully recognised that copper, lithium, nickel etc are needed to support the technological advances to decarbonise the world. The shift of funds to ESG and sustainable themes is a huge opportunity and mining is a central theme of most sustainable frameworks. Impact investors, by and large, are permitted to invest in mining: they just choose not to! In virtually all my conversations with these groups, there is a common challenge:

“Give us a means to credibly track ESG and we can start to invest.”

This isn’t just an exercise in maintaining the status quo: this is an opportunity of epic proportion. Imagine if this small industry of less than 3,000 public companies accepted the inevitable and started to disclose in a standardised format that facilitated internal and external discussion, acknowledged the credibility gap and therefore encouraged a 3rd party assessment. This would give investors and other stakeholders the confidence and conviction needed to begin to believe in the changes taking place.

Imagine what the results would be:

- conviction would increase

- confidence in the sector would grow

- cost of capital would likely reduce

- long term investors, such as sustainable funds, would start dipping their toe in

- labeled and green bonds would emerge

- managements incentivised to perform relative to their peers

- cost efficiencies will materialise as less energy is used, more efficient working practices are employed

- new investment in technology would have impacts on business functions, environment and social

- the industry would begin to inspire younger persons for employment

- local stakeholders would have a transparent means to engage with operators

- ….and my favorite of this list in the last week is the differential of metal pricing, facilitated by blockchain.

This is not naive small talk, it is a business imperative. Imagine the alternative where investment portfolios, government policy and industry move on without us. How long will licensing negotiations extend without a credible dialogue with NGOs and policy-makers on climate impact? It is only a matter of time before voting of directors extends right across the spectrum to force change based on ESG metrics. We are already experiencing early evidence of the positive impact credible disclosure can make.

I was encouraged nearly two years ago by leading stakeholders of the industry to find a solution to disclose ESG. Digbee ESG makes disclosure easy, providing a means for all companies to be ESG accredited following a 3rd party assessment and it provides a means to communicate this to all its stakeholders.

Mining offers so much to this world but for it to really benefit, it needs to find a level of credibility with which society, stakeholders and investors can rely upon.

Digbee provides its frameworks for free to any company, the blueprints are there for all to disclose. Our goal is to encourage the whole sector to get on board, prove this industry embraces a more sustainable future so that our children can demonstrate that the actions we took encouraged a vibrant, attractive and highly valued industry in a new world.

Learn more about the Digbee team

Pick a date to demo Digbee ESG