As the mining industry shifts decisively into third gear, investors are no longer focused solely on geology or commodity price optionality. Capital is being allocated through a far more exacting lens, one that recognises the reality of mine development risk and rewards management teams that can prove they are prepared for it.

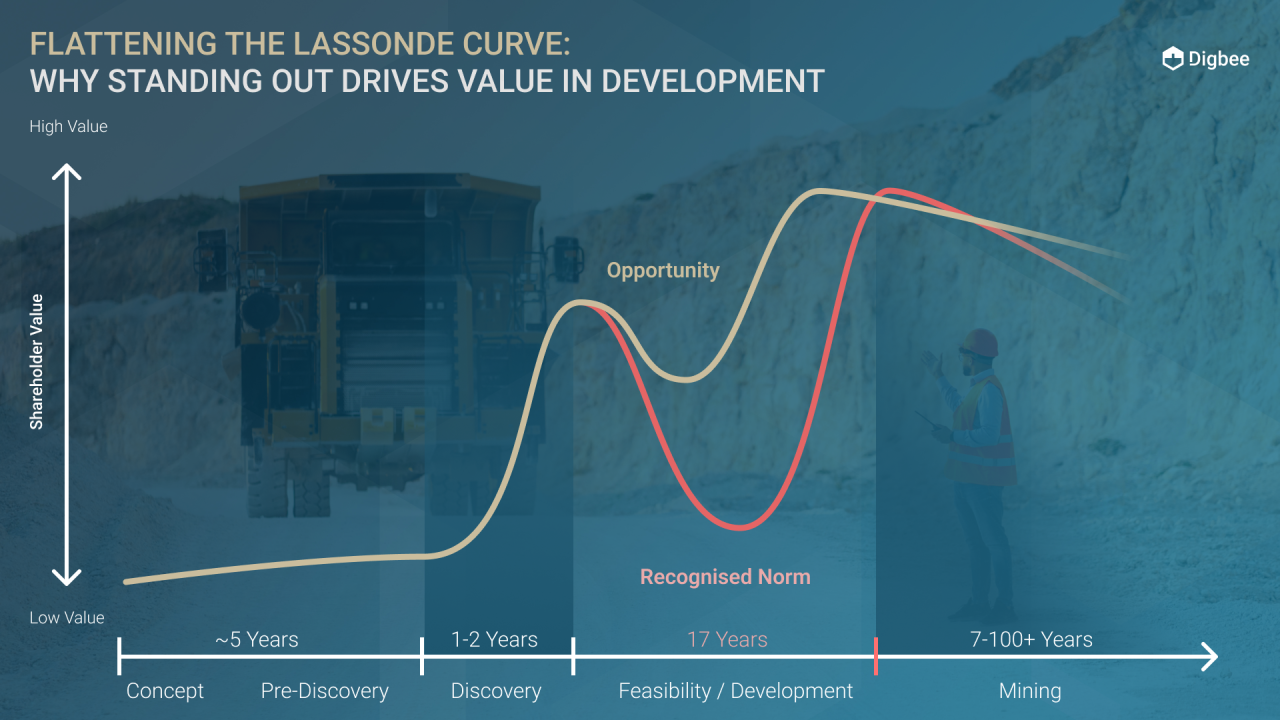

Few concepts have shaped mining narratives more enduringly than the Lassonde Curve, first articulated by the legendary Pierre Lassonde. For decades, developers have used this curve to explain how value should rise as projects move from discovery, through development, and into production. In theory, as uncertainty reduces and cash flow approaches, valuations should accelerate.

In practice, the statistics tell a more sobering story.

Despite strong intent and technical competence, 83% of mining projects fail to deliver on budget and schedule, a figure highlighted by McKinsey and reinforced publicly by Worley’s VP, Darryn Quayle. Markets, astute as ever, tend to sense this danger well before first production. As development capital tightens, optimism bias fades, and projects approach construction, the expected value uplift is frequently reversed.

This is the true valley of death.

“In mining, discovery creates excitement, construction reveals truth. The valley of death is simply where optimism runs out and evidence finally matters.”

Darryn Quayle, VP, Worley

Instead of re-rating, companies often face depleted balance sheets, strained debt covenants, and the need for deeply dilutive equity raises simply to keep financiers at bay. The irony is that these setbacks are rarely driven by geology or engineering alone. More often, they stem from inadequate preparation for non-technical risks, social licence, governance, stakeholder trust, permitting confidence, and credibility with capital providers.

Bull Markets Are Never Linear, Value Is Defined in the Down Cycles

Structural demand growth, chronic underinvestment, and rising geopolitical tension continue to underpin a compelling long-term outlook for the mining sector. But history is unequivocal: bull markets are never smooth. They are punctuated by periods of weakness, cost pressure, and loss of momentum, as recent years across the technology sector have clearly demonstrated.

In mining, these phases are often characterised by more projects advancing at once, intensifying competition for skilled people, and accelerating cost inflation across labour, equipment, energy, and services. These conditions are not anomalies; they are predictable features of the cycle. Yet there is little evidence that either the sector or the financial community has meaningfully adapted behaviour in response.

Too often, development strategies remain anchored to optimism bias: best-case economics, insufficient contingencies, and late recognition of social, permitting, or execution risks. When cycles turn, even temporarily, markets respond quickly, capital discipline tightens, and value erodes at precisely the point where confidence matters most.

Those that stand apart take a different approach. They remove optimism bias early, publish economic studies grounded in realistic assumptions and appropriate contingencies, and engage meaningfully with communities well before development decisions are locked in. Most importantly, they identify potential risks before capital is fully committed and set out credible mitigation strategies that investors, lenders, and regulators can interrogate and trust.

It is during these periods of contraction, not expansion, that management quality is truly revealed. Preparedness becomes the defining differentiator, allowing some companies to navigate volatility, protect value, and progress with confidence, while others are forced into delay, and dilution.

Where Value Is Really Won or Lost

Standing out from this crowd is not only advisable, it is entirely achievable.

Companies that identify, evidence, and mitigate these risks early; that build durable relationships with communities, regulators, and investors; and that can prove responsibility rather than promise it, fundamentally change how the market perceives them. The result is a powerful double benefit:

- Avoiding the discounted fundraises that erode shareholder value and define so many development stories.

- Earning a management premium, where credibility, preparation, and execution command higher valuations.

This is not theoretical. Look at the consistent approaches taken by Lundin family of companies, Champion Iron, Agnico Eagle, and B2Gold. Different assets, different jurisdictions, but a common thread: disciplined risk management, early engagement, and a culture of preparedness that the market trusts.

From Optimism Bias to Investable Confidence

Digbee exists to help development companies flatten the Lassonde Curve, reducing the depth and duration of the valley of death by replacing optimism bias with evidence-based readiness. By independently assessing and validating how non-technical risks are being managed, Digbee enables companies to stand out, build confidence earlier, and align with how investors now make decisions.

Proven responsibility has become one of the few tools genuinely within management’s control. While many drivers of value are dictated by commodity price cycles and external market forces, predictability, preparedness, risk mitigation, and credibility are not. Used effectively, they allow strong management teams to introduce greater certainty into their development pathway, creating real value, or avoiding costly pitfalls, at precisely the point in the cycle where investors price risk most acutely and outcomes are most often decided.