Digbee welcomes and encourages insights and experience shared from the global Digbee Expert Community. This article was prepared by Edmund Sides in his personal capacity. The opinions expressed in this article are the author’s own and do not necessarily reflect the views of Digbee.

Introduction

Over the past decade, investors have become increasingly concerned about how their investment strategy and decisions affect the physical and human environment around the globe. This has led to an increasing focus by investors and their advisors on the environmental, social and governance (ESG) aspects of company activities and investment funds. Organisations involved with setting standards for public reporting, such as the Committee for Mineral Reserves International Reporting (CRIRSCO) and the Pan-European Reserves and Resources Reporting Committee (PERC), are currently looking at ways of providing additional guidance to mining professionals with regards to reporting on the ESG aspects of mineral projects.

The author is the current Secretary of PERC, and one of PERC’s two representatives on CRIRSCO. This article provides his personal perspective on the subject of ESG disclosure in relation to mining projects, together with an overview of some recent developments in this regard. Comments made in this article do not necessarily reflect the views and policy of PERC and CRIRSCO.

Background

At a special event to launch the UN’s Principles of Responsible Investment (PRI), which was held at the New York Stock Exchange in April 2006, the Secretary General Kofi Annan stated that: “while finance fuels the global economy, investment decision-making does not sufficiently reflect environmental, social and corporate governance considerations -– or put another way, the tenets of sustainable development.” The six Principles for Responsible Investment are a voluntary and aspirational set of investment principles that offer several options for incorporating ESG issues into investment practice. At the time of the launch of the Principles, an independent body called the PRI (see: www.unpri.org) which is supported by, but not part of, the United Nations, was set up to promote their adoption by investors.

Since the Principles were launched in 2006, they have attracted a global signatory base (currently numbering over 3,000) which now represents a majority of the world’s professionally managed investments. In following the Principles, investment managers often need to make a choice between engagement (working with companies to develop strong ESG practices) or divestment (walking away from companies with poor ESG practices). In either case, there is a clear need for companies to accurately disclose their current ESG performance in a format that will allow investors to compare different companies with one another and track the performance of individual companies or projects over time.

ESG aspects of mining projects

Consideration of environmental and social impacts has been a standard part of the permitting process for new mining projects in most jurisdictions around the world for some time, usually in the context of submitting environmental and social impact assessment (ESIA) reports in order to obtain environmental permits for new developments. ESIA reports provide details of the results of baseline studies which document the present status of a project area and identify natural, community and cultural features; how they may be affected by mining; and measures to be taken to avoid or mitigate adverse impacts.

In recent years there have been increasing demands by investors for mining companies to provide more information about the ESG aspects of mining projects reflecting a general change in attitudes by both the investment community and the general public. The use of the ESIA process has been, and is likely to remain, the primary process used in the management of the environmental and social impacts of a mining project, however, in future such assessments will need to be integrated into the overall context of ESG so as to provide a closer link with the decision making processes involved in the development and operation of mining projects.

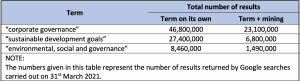

In order to obtain evidence to confirm that interest in ESG aspects is of increasing importance, the author used Google Trends (trends.google.com) to investigate trends in searches on Google for topics and terms related to responsible investment since the start of 2004. Quantitative data on the relative “popularity” of several topics on a month by month and worldwide basis, from January 2004 up to March 2021, were downloaded from Google Trends. A monthly average was then calculated for each 3-month period and time trends plotted. In the context of Google Trends, a topic is defined as a group of terms that share the same concept, rather than being a specific search term. The results obtained for three selected topics is summarised in graphical form in Figure 1 below.

The values on the Y-axis of the graph represent an index ranging from 0-100 where 100 represents the peak popularity for the selected region and time period considered. A value of 100 is the peak popularity of the term, whilst a value of 50 means that the term is half as popular. The results presented in the figure indicate that there has been a strong upsurge in interest in the topic of “Sustainable Development Goals” from 2015 onwards, and a more recent upturn in interest in the topic of “environmental, social and corporate governance” from early 2019 onwards. Whilst this analysis is not necessarily representative of the interests of the investment community, the results highlight the fact that for Google users the topic of ESG is of increasing interest in recent years, whereas interest in the topic of corporate governance shows a slight decline over the past decade.

Unfortunately, Google Trends does not allow trends in interest for combinations of topics or search terms to be analysed. In order to confirm the level of interest in the three topics represented in Figure 1 in the context of mining, the author performed several searches on Google to determine the number of results returned for different combinations. The results presented in Table 1 below indicate that in reality, the topic of corporate governance is of overall greater interest than the other two topics with a very high level of interest in the context of mining as well. Interest in SDGs and ESG appears to be of more general interest with a lower proportion of results when combined with “mining”, however, the level of interest in the context of mining is still very significant.

The results of the background research performed by the author confirm that there is increasing general interest in the topics of sustainable development goals (SDGs) and ESG and this is also true in the context of mining. The rise in interest in the topic of ESG appears to have started around the beginning of 2019.

Requirements for disclosure of ESG aspects in mining projects

Reporting of ESG information related to mining projects commonly occurs in two forms:

- Disclosure by publicly listed companies for the purposes of informing investors and their advisors, which must be done in accordance with the relevant national legislation and stock exchange regulations. Such disclosures are mostly done in compliance with one of the CRIRSCO family of reporting codes or standards. These include the National Instrument 43-101 (NI 43-101) legislation in Canada and the JORC Code in Australia.

- Submissions made to government departments to support applications for mining, environmental and other permits required in order to develop, or continue operating, a mining project. In some cases these types of submission will not be made publicly available, however, in other situations such as a planning inquiry, they would be available to the public.

In both cases, it is expected that the disclosures should identify aspects of the physical and human environment that may be affected by mining-related activities and present plans for mitigating any risks and monitoring and controlling the effects of mining.

With respect to public disclosure by listed companies, a good example is the requirement for Canadian listed companies publishing NI 43-101 Technical Reports to include a section entitled “Environmental Studies, Permitting and Social or Community Impact” which should discuss the results of relevant studies as well as the permitting and other requirements with respect to waste and tailings disposal, mine closure and social or community-related aspects. Similarly, the November 2019 version of the CRIRSCO International Reporting Template includes a Section entitled “Sustainability Considerations” which specifies that: “Public Reports should discuss environmental, social, health and safety impacts that are expected during development, operation and after closure.” In addition, the general principle of Materiality, which applies to all of the CRIRSCO codes, requires that a Public Report should: “contain all the relevant information which investors and their professional advisers would reasonably require, and reasonably expect to find” in order to allow them to make a reasoned and balanced judgement with respect to actual or potential investments in a project.

A pioneering initiative in raising awareness of the need for improved reporting of ESG aspects in relation to mining projects was the release of the SAMESG guideline in South Africa in 2016 (see: https://www.samcode.co.za/samcode-ssc/samesg). The SAMESG guideline covers the reporting of ESG parameters in South Africa and complements the SAMREC Code – the South African CRIRSCO-compliant reporting code. It was specifically developed in order to provide a standardised, systematic and orderly framework for public reporting of ESG parameters in the extractive industries (inclusive of solid minerals and oil and gas projects), and is currently applicable to extractives companies listed on the Johannesburg Stock Exchange (JSE). The SAMESG guideline has been widely recognised as leading the way in terms of reporting ESG aspects related to minerals projects and provides a basis for further development internationally.

Recent developments

Despite the requirements noted above, there has been increasing concern amongst investors and mining professionals about the need for more attention to be paid to the reporting of ESG aspects of mining projects in a clearer and more transparent manner so as to facilitate comparisons of different companies and projects from a sustainability perspective. Wider public concerns have also been raised by several recent high profile incidents related to mining activities, including the Brumadinho tailings dam disaster in Brazil in January 2019 and the destruction of the Juukan Gorge cave shelters in Australia in May 2020.

Over the past couple of years, several events have been organised in order to promote discussion on the topic of ESG in mining. This included a virtual conference on the topic of “Responsible Raw Materials” which was held in May 2020 and two virtual ‘roundtable’ discussions on the inclusion of ESG aspects in reporting of mineral deposit estimates and exploration results globally which was held in January 2021. Recordings of the presentations made at these sessions are available on YouTube and can be accessed from the www.responsiblerawmaterials.com website.

At the roundtable discussion held in January 2021, it was noted that at the 2020 CRIRSCO AGM, PERC was asked to take the lead on improving the guidance on reporting on ESG aspects. This is now being done in the context of an update to the PERC Reporting Standard which is based on CRIRSCO’s International Reporting Template – the common reporting framework that CRIRSCO members use as the basis for developing their own codes and standards. PERC is currently (April 2021) finalising an update to the PERC Reporting Standard which incorporates several general changes that were introduced in the CRIRSCO International Reporting Template in November 2019. This update is also providing the opportunity to include additional guidance on the reporting of ESG aspects.

The proposed changes related to the reporting of ESG aspects will build on the work done on the SAMESG guideline, and it will highlight the importance of reporting on any ESG risks and uncertainties associated with a minerals project from the initial exploration stage onwards. It is anticipated that the updated version of the PERC Reporting Standard will be issued in mid-2021, and in line with CRIRSCO requirements, will be circulated to other CRIRSCO members prior to its adoption by PERC. Once finalised and accepted, the guidance on reporting of ESG aspects contained in the updated version of the PERC Reporting Standard will provide an example that other CRIRSCO members can refer to when updating their own national/regional codes and standards.

Conclusions

As discussed above, in recent years there has been an increasing interest in responsible investment with investors and fund managers trying to ensure that their investments will support sustainable development around the world. In this context, there has been increasing demands by investors for mining companies to provide more information about the ESG aspects of mining projects. CRIRSCO and its member organisations which are responsible for developing and maintaining international mineral reporting codes are aware of this need and are taking steps to provide additional guidance on reporting on the ESG aspects of mining projects.

A large number of very useful standards and guidelines related to ESG related aspects of mining and other projects already exist, including for instance:

- The Global Industry Standard on Tailings Management (https://globaltailingsreview.org/global-industry-standard/)

- The Mining Association of Canada’s Towards Sustainable Mining standard (https://mining.ca/towards-sustainable-mining/)

- The Equator Principles (https://equator-principles.com/)

Many mining professionals may feel overwhelmed by the thought of additional rules and guidance being developed for them to follow. It is to be hoped that the additional guidance on reporting of ESG aspects, which will be included in the international mineral reporting codes, will highlight the existing requirements of these codes to inform investors about material issues and risks. Greater awareness of the fact that ESG aspects should be dealt with in this context will help to support more consistent ESG reporting so as to assist the investment community in assessing and comparing ESG aspects of different mining projects and companies.