The mining industry is filled with pleas for action – from governments to speed up permitting, from investors to recognise the urgency of critical minerals, from banks to take more risk, and from conferences to bring in new capital.

But here’s the uncomfortable truth: none of this will make a meaningful difference unless the sector first addresses the real issue – itself.

It’s not enough to hope the commodity cycle will turn. Gold prices are near all-time highs, yet many gold equities continue to underperform. If that doesn’t serve as a wake-up call for the rest of the sector, what will?

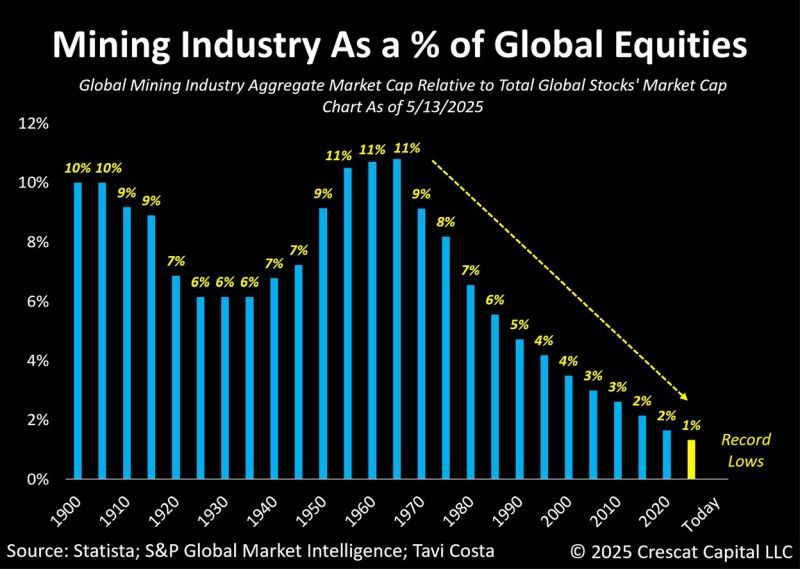

The decline in relevance is stark. Mining once made up more than 10% of global equity indexes – today it accounts for less than 2.5%. Valuations have collapsed accordingly, with sector-wide cash flow multiples falling from double digits to below 4x. In the eyes of many institutional investors, mining is no longer just underweight – it’s considered irrelevant.

And yet, within this uncomfortable truth lies a massive opportunity – one that requires bold, proactive leadership. A handful of companies have already broken from the pack by embedding responsibility, preparing early, and communicating with transparency. These companies are raising cheaper capital, securing stronger partners, and trading at premiums. The path exists – but it demands a shift from old habits to new discipline.

The Data Is Clear — And It’s Damning

According to McKinsey’s The Capex Crystal Ball, just 17% of mining projects in the last 15 years were delivered on time and on budget. The average cost overrun was over 40%.

This is not a commodity price issue. It’s not just a funding gap. It’s a confidence crisis. Investors, governments, communities, and offtakers are all wary – not because they don’t understand the need for critical minerals, but because they don’t believe most mining companies can deliver responsibly.

The Trust Deficit

Most development-stage companies still lead with the same outdated formula – a few maps, exciting geology, some long-term upside, and a glossy feasibility study based on thousands of variables. But they fail to answer the single most important question:

Can you actually build this project – on time, on budget, and with trust from the people and institutions that matter?

Too often, the answer is no. And investors can see that from a mile away.

What’s missing is a credible demonstration of how risks – not just geological and technical, but also environmental, social, regulatory, and governance-related – are being actively identified and mitigated. And more importantly, how management plans to stay ahead of these risks as the project advances.

The narrative must shift – dramatically – from technical optimism and future upside to disciplined risk preparation and delivery. Investors, particularly those outside the mining sector, don’t respond to grade, tonnes, and NPVs alone. They want to see that management understands and is actively mitigating the full spectrum of risks. They want to know whether this team has the operational discipline, stakeholder engagement, and governance structure to keep the project on track.

Where’s the visibility on:

- Internal team capability and execution history?

- Board and management alignment?

- Water, waste, and biodiversity risks?

- Permitting and community relationships?

- The culture and governance needed to deliver under pressure?

This is the story that must be told – clearly, credibly, and repeatedly. Until that happens, capital won’t flow – regardless of how many critical mineral headlines appear on the front pages.

The Industry’s Conferences Reflect the Disconnect

A Tier 1 communications group recently shared with me that they had been exploring a new critical minerals conference. In speaking to dozens of mining companies, nearly all said their top issue was capital access – and their top request was for new institutional investors to attend.

That request itself speaks volumes. If current investors aren’t engaged, it’s not because they don’t exist – it’s because the message hasn’t changed. The content of the conversation is the problem. Not the venue.

Even the Capital Providers Are Struggling

RCF, one of the most respected investors in the space, recently abandoned efforts to launch a new mining credit fund. The reason? Asset allocators couldn’t reconcile ESG frameworks with the mining sector.

Yes, they increasingly understand the energy transition and critical mineral imperative. But they still don’t see enough evidence that good practices and responsible operations can reliably mitigate risk.

And that’s the key – it’s not about greenwashing or broad claims. It’s about real, verifiable change.

There are tools to support this:

- Consolidated, updated global standards specifically tailored to mining

- Independent verification and transparent assessments

- Modern frameworks that bring sustainability into operational and investment decision-making

But the opportunity to transform the industry will remain out of reach unless mining companies begin to solve their underlying issues – by embedding risk awareness into strategy, building internal capacity, and communicating transparently.

Learn From Steel

The steel industry offers a compelling parallel. It’s also cyclical, capital-intensive, and once shunned by ESG investors. But it has moved.

Nippon Steel is investing $6 billion in electric arc furnaces. Nucor’s CEO, in a recent McKinsey interview, spoke about how culture, preparation, and long-term thinking are creating a sustainable competitive advantage.

The result? Steel trades at 3–4x the multiple of the mining sector on earnings and cash flow. That’s not an accident. It’s the return on credibility.

There Are Examples in Mining Too

Take Marimaca Copper, for instance. Still in pre-production, but already demonstrating a strong internal culture, credible risk mitigation, and thoughtful engagement. It’s ahead on permitting, attracts strong offtake partners, raises capital at low-single-digit costs, and trades at a premium.

It’s not perfect – but it’s trusted. And in this market, that’s the difference.

Compliance Isn’t Enough — Responsibility Is the Answer

There’s a world of difference between being compliant and being responsible. Compliance is ticking boxes. Responsibility is earning confidence through action.

Responsible companies:

- Identify risk early

- Prepare thoroughly

- Align internal governance with operational delivery

- Communicate clearly and transparently to all stakeholders

This is what drives down risk. This is what attracts capital. This is what separates the 17% from the rest.

Conclusion: The Industry Must Lead

The mining sector can no longer afford to point fingers at governments, investors, or conference organisers.

We must fix the foundation:

- Get real about our delivery track record

- Embed a culture of preparation and responsibility

- Tell a better, truer, and more useful story to capital markets

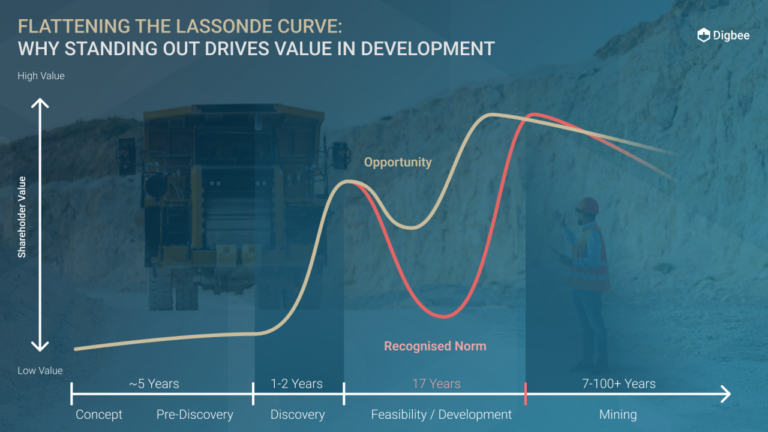

The Lassonde Curve doesn’t have to be a death valley. It can be flattened – through leadership, discipline, and trust. And it doesn’t stop at development. The value of being trusted compounds over time. Producing companies that continue to demonstrate operational discipline, governance maturity, and stakeholder credibility not only deliver returns – they trade at premiums and enjoy lower-cost capital.

As Marcelo Kim of Paulson & Co. said when asked why they continue to own Agnico Eagle: “We’d rather pay a high multiple for a company where we’re comfortable with what they’re doing.” That’s the reward for responsibility.

The tools exist. The need is urgent. The opportunity is massive. But the responsibility to act lies squarely with us.